Pay off your debt first. Freedom from your debt is worth more than any amount you can earn. – Mark Cuban.

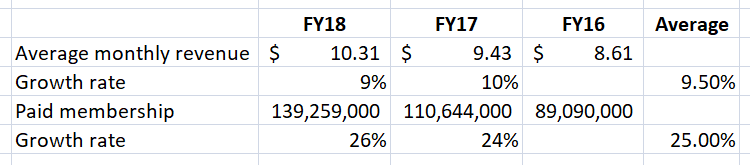

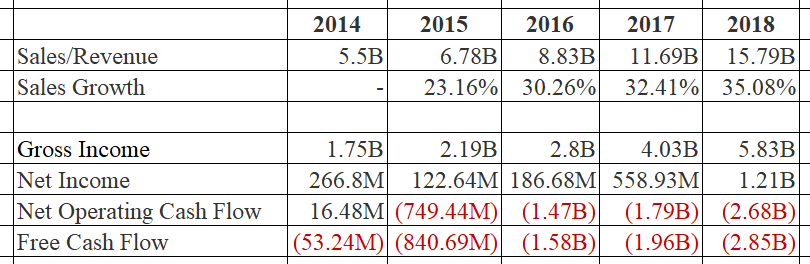

It is relatively easy to predict the future revenue of Subscription-based companies. We can multiple its subscribers and average subscription price to get expected revenue. Netflix, Inc. is the world’s leading internet entertainment service with little over 139 million paid memberships in over 190 countries enjoying TV series, documentaries and feature films across a wide variety of genres and languages. In 2018, Netflix’s revenue was $15.7 billion and its average monthly revenue per paying membership was $10.31.

| 2018 | |

| Subscribers | 139,259,000 |

| Total Revenue | $15,794,341,000 |

| Average Price | $10.31 |

Given the above figures, can we predict Netflix’s revenue in the year 2028? Well, let’s find out. The only numbers we need is its expected total number of subscribers and average subscription price. The best way to get those two numbers is to get their respective growth rate and apply those growth rates to the current actual numbers. Now, let’s look at the historical data to compute the growth rate.

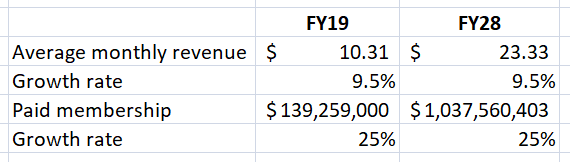

You will get over a billion members and average monthly revenue of $23.33 (figure below) in FY28 if you apply the average growth rate. Even though Netflix’s core strategy is to grow their streaming membership business globally within the parameters of their operating margin target, it is highly unlikely that in FY28 they will have over a billion paid members. Nevertheless, the average monthly revenue might be possible dependent on inflation and other factors. These two numbers are inversely proportional to each other. It is hard to grow them both at the same pace. You have to either sacrifice average revenue to get the paid members or vice versa.

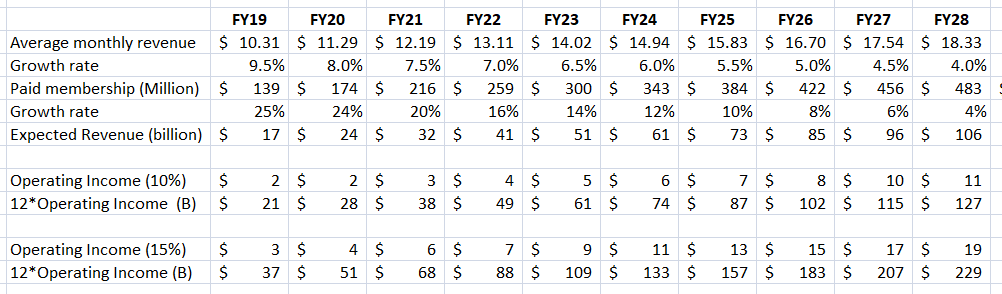

So, after applying some modesty to our growth rate, we have estimated 483 million paid subscribers and $18.33 average revenue per member per month in the year 2028 (figure below). There is no science to the assumptions below. It is purely a subjective guess. Just a small change in those rates will change the total number dramatically given this long time frame. Thus far, Netflix is able to achieve exponential growth, but it will be seemingly impossible to extrapolate the historical growth into the future. We are so much affected by availability bias that we always run into this issue.

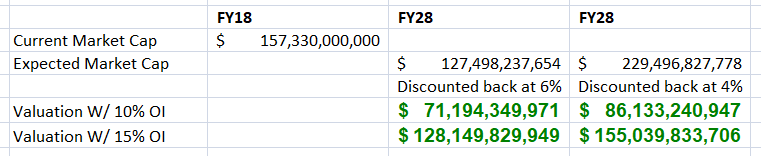

Netflix valuation in the year 2028 is in between $71 and $155 billion. The most optimistic valuation of $155 billion in 2018 is also above the current market capitalization of $165 billion. Netflix is expensive at the current price! There are a lot of factors that need to go absolutely perfect to justify the current valuation. One can obviously argue that the assumptions applied while computing future revenue are wrong. We have to agree to that not because we haven’t use the right assumptions but because assumptions themselves are wrong by nature. Forgetting the future valuation, if you just look at the current financials, which avoids assumptions altogether, it is way expensive as well. I am sorry to the current investors. Apparently, I am one of them!

Nature of the business

Netflix has changed the way we look at entertainment. They were apt to leverage the new technology to serve their customers. They were quick to understand human nature, which is being lazy, and seeking comfort in every way and they infused entertainment in this raft, which floated with the human tide. This seems like a great business strategy.

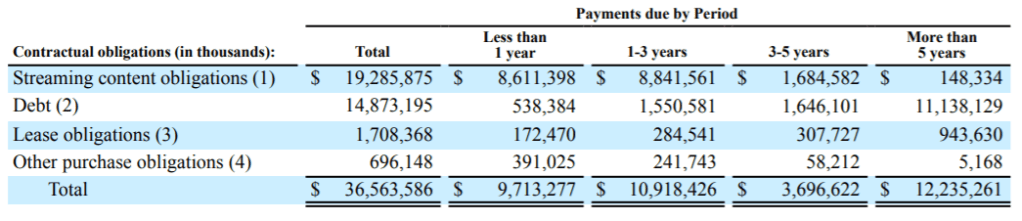

At present, almost 85% of the total revenue goes to the cost of revenue, which are related to content amortization relating to their existing and new streaming content, including more exclusive and original programming. The long-term and fixed cost nature of Netflix content commitments may limit their operating flexibility and could adversely affect their liquidity and results of operations. As of December 31, 2018, they had approximately 7,100 full-time employees, of which approximately 6,900 supported their streaming segments.

Streaming content obligations increased $1.6 billion from $17.7 billion as of December 31, 2017 to $19.3 billion as of December 31, 2018 primarily due to multi-year commitments associated with the continued expansion of their exclusive and original programming. Streaming content obligations include amounts related to the acquisition, licensing and production of streaming content. An obligation for the production of content includes non-cancelable commitments under creative talent and employment agreements and other production related commitments.

Netflix is heavily indebted. Long-term debt, net of debt issuance costs, increased $3,861 million due to long-term note issuances of $1,900 million in April 2018 and $800 million and €1,100 million in October 2018.

Netflix is burning a lot of cash. It is spending those cash on content creation. And it seems like it will continue to do so for a long time. Netflix offers its members unlimited viewing of TV series and films. The only way to retain the current member and to acquire new customers is to create more appealing contents, which need more cash.

Netflix pays 3% of the revenue in interest expense. Interest expense for the year ended December 31, 2018 consists primarily of $409 million of interest on their Notes. The increase in interest expense for the year ended December 31, 2018 as compared to the year ended December 31, 2017 is due to the increase in long-term debt.

Because of the blood red cash flow, it is very hard to apply the discounted cash flow valuation methodology. Netflix should generate a ton of cash in the future (current negative cash plus its interest) to justify its sky-high valuation.

Final Thought

Netflix, being first in the market, enjoys network effect. If some user is a Netflix subscriber then his/her friends are most likely will be Netflix subscribers. If some close friends or family talk about some of Netflix’s original shows or movies, people feel tempted to subscribe to Netflix and watch the shows/moves to conform with the public. This is an incredible force, which can be extremely profitable to businesses. I am one of the examples of it. I did not want to be left out, therefore, I had to subscribe to Netflix to watch Narcos because all of my friends are watching it and most importantly, talking about it. If you haven’t watched it yet, you should! It is an amazing show.

I know investors are quite unrealistically optimistic about the future of the company. Here is how I feel about it:

- The entertainment industry is evolving and if there is any company which is ready and able to grab those opportunities, it is Netflix.

- The cost of revenue is quite high with high fixed cost. Netflix will take advantage of economy of scale once it reaches the critical break-even point. Everything above that is profit and the net margin will surely go up.

- The beauty of high fixed and upfront cost business is that the first player to enter the game will take all the advantages. There will be stiff competition for the newcomers.

- There is a big chunk of the market yet to be explored, especially developing countries. (Netflix is banned in China, Iran, and North Korea.)

However, there is no data to support any of the above expectations. Another consoling point I enjoy is that my Netflix holding has turned quite profitable that if the current market price halves, I will still be in profit. So, I have a little bit of cushion to rely on and be optimistic about my gambling with it. It is a part of my overconfidense. I prefer to call it gambling because I have given up on another cash-rich media giant Disney (Market Cap – 236 billion) to be with heavily indebted Netflix (Market Cap – 165billion).

Disclaimer: Long position on Netflix.