“If you do what you’ve always done, you’ll get what you’ve always gotten.” ― Tony Robbins.

Macy’s Inc (NYSE: M) sells a wide range of merchandise, including apparel and accessories (men’s, women’s and kids’), cosmetics, home furnishings, and other consumer goods.

Source: Fortune

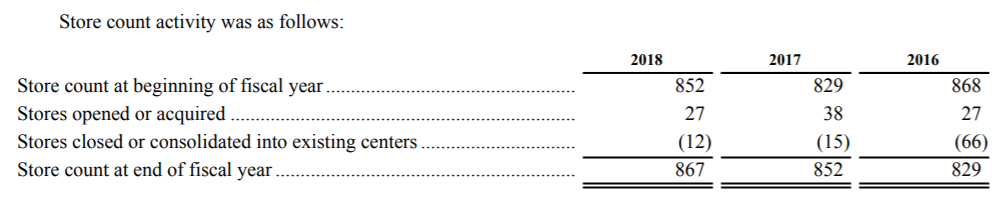

At the end of the fiscal year 2018, Macy’s has 867 stores. Although Macy’s is one of the nation’s largest retailers, they have numerous and varied competitors at the national and local levels. One of its biggest rivals is Amazon. Not just Macy’s but all the brick and mortar stores are losing share to Amazon.

In the last five years, Macy’s stock is down almost 63%. At the same time, the Dow Jones Industrial Average is up 54%. If you had invested $10,000 in Macy’s five years ago, you will have only $4,700!

Source: Yahoo

Financial Overview

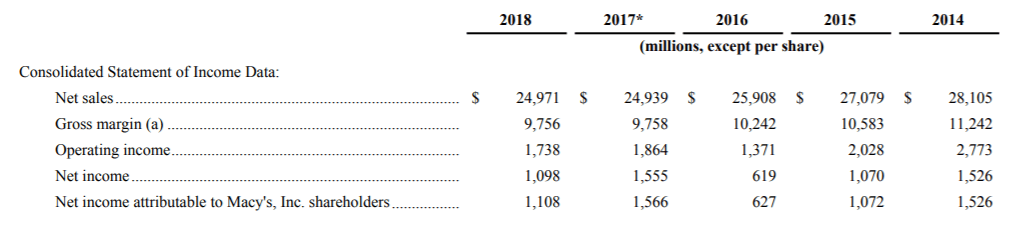

Macy’s net sales for 2018 were $24.9 billion, an increase of $32 million, or 0.1%, from 2017, which included the 53rd week of operations. Digital sales continued to be strong in 2018 and experienced double-digit growth.

During 2018, the Company announced a retail store strategy for Macy’s that focuses on identifying a scalable investment strategy for all of the brand’s stores, improving the customer’s experience and growing total sales profitably. This strategy includes categorization of the Company’s Macy’s stores into three groups: Flagship, Magnet, and Neighborhood stores. Therefore, 2018 saw the execution of the Company’s North Star strategy which resulted in healthier stores and continued e-commerce growth. Here are the quick highlights.

- Net sales increased by 0.1% compared to 2017, which included the 53rd week of operations.

- Comparable sales on an owned basis increased 1.7% and comparable sales on an owned plus licensed basis increased 2.0%.

In 2018, the Company continued to execute on its real estate strategy through both monetization and redevelopment of certain assets. As an initial step, the Company developed a plan in 2018 that reduces the complexity of the upper management structure to increase the speed of decision making, reduce costs and respond to changing customer expectations.

On September 18, 2018, the Office of the U.S. Trade Representative announced that the current U.S. Administration would impose a 10% tariff on approximately $200 billion worth of imports from China into the U.S. effective September 24, 2018, which was expected to increase to 25% starting January 1, 2019. This will negatively affect sales, although Macy’s have no control over it.

On a comparative basis, the 2018 rate reflects the Company’s lower federal income tax statutory rate of 21% as compared to 35% resulting from the U.S. federal tax reform enacted in 2017. This is a one-time positive impact.

Management

Jeff Gennette has been Chief Executive Officer of the Company since March 2017 and Chairman of the Board since January 2018; prior thereto he was President from March 2014 to August 2017, Chief Merchandising Officer from February 2009 to March 2014, Chairman and Chief Executive Officer of Macy’s West in San Francisco from February 2008 to February 2009 and Chairman and Chief Executive Officer of Seattle-based Macy’s Northwest from February 2006 through February 2008.

I see no extraordinary expertise in the top leaders. They all seem old dogs with all old tactics.

Valuation

Based on the 2018 financials, it’s P/E is 6. It seems a really good deal in the current overvalued market.

Based on its assessment of current and anticipated market conditions and its recent performance, the Company’s 2019 guidance assumptions include the following:

- Net sales are estimated to be approximately flat to 2018

- Comparable sales on both an owned and owned plus licensed basis are estimated to be flat to up 1.0%.

- Gross margin rate is estimated to be down moderately in the first half and down slightly in the second half of the year

- Net income attributable to Macy’s, Inc. shareholders for 2018 was $1,108 million, a decrease of $458 million from $1,566 million in 2017.

The year 2019 will be flat if not down. Most probably down, if the ongoing trade war with China goes on full-fledged.

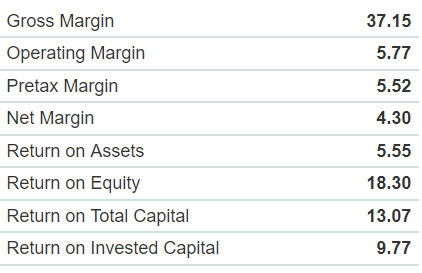

Although the price of just $6.6 billion is pretty attractive, the problem is its falling sales and very low net margin. The net margin is at 4.3%. If the trade war goes on a bit longer, it will drag that towards red. The current market capitalization is almost fully supported by their total current assets of $7.5 billion of which $5.5 billion in inventory. Their Net Property, Plant & Equipment is valued at $6.6 billion.

At the current rate, Macy’s pays a 7% dividend per year. This is an extremely favorable situation, but will it last for 10 years? I doubt it. Macy’s is constantly selling their assets and their net cash flow is sustainable, but that will not continue forever.

In the current market situation, a company with $24.9 billion sales, and $1.1 billion net income is offered at $6.6 billion is certainly a bargain.

Final Thought

As part of the Company’s commitment to increased productivity to fund investment in the business, in February 2019 the Company launched a comprehensive, multi-year program focused on growing its profitability rate by improving productivity across the enterprise. The program includes initiatives to improve margin through enhanced inventory planning and operations, supply chain efficiencies, pricing optimization, improved private brand sourcing, and customer acquisition and retention strategies.

I believe Macy’s strategy is not even directionally correct. In none of their strategy, they are focusing on online sales. This is proved by their website (see below). Macy’s website is not at all robust. It should not take a bit to copy the proven concept from other successful online retailers like Amazon or Alibaba. Macy’s is not at all serious about the online market opportunity. And I believe this kill Macy’s.

The current and past management is directly responsible for the downfall of Macy’s. They are not quick to adapt to the changing business environment. And still, they are reluctant to change. With the current management and their strategy, all we can do is pray for the softer landing of Macy’s. At this pricing, if tech-focused management heads the company, investors should lineup to buy their shares. And I will be one of them.

Disclaimer: No position.