Top 15 Things Money Can’t Buy – Time. Happiness. Inner Peace. Integrity. Love. Character. Manners. Health. Respect. Morals. Trust. Patience. Class. Common sense. Dignity.

– Roy T. Bennett.

The obvious parts of Finance, Money and Investing are:

- Spend less than you earn

- Invest the difference

- Diversify

- Long-term.

Apparently, these obvious parts gets ignored all the time. People mistake simple for inferior, therefore they try to complicate things unnecessarily. People think that if it is obvious it can not be powerful; so they spend time doing that are less obvious and much more complicated. Matter of fact, these are the only fundamentals of finance, money and investing.

Everyone wants to know what else? There isn’t any!

It is similar to Health, where a lot of key to health, put a side bad luck and genetics, are diet and exercise. That answer is too simple and not a fun answer to hear, therefore people ignore that and try to look for a magic pill.

Let’s examine each one of it in detail.

1 – Spend Less Than you Earn

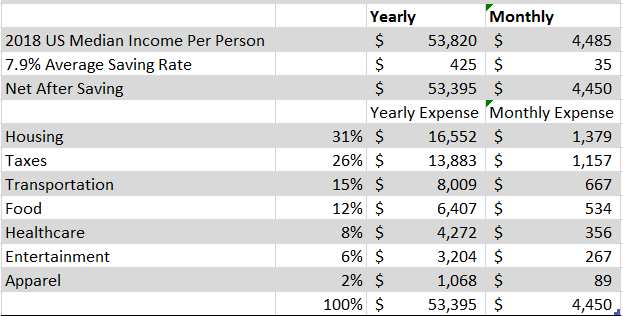

In 2018, United States of America’s median income per capita was $53,820. According to Statistics, in January 2020, the personal saving rate in the U.S. amounted to 7.9 percent. Based on the above figure, the average saving per person comes to $425 per year or $35 per month.

The average saving of $35 per month seems seemingly too easy. A pair of Jeans or 10 Starbucks Lattes costs more than that.

What makes it difficult?

Even though it seems too easy to save $35 a month, the difficulty lies in the consistency. $35 per month seems too trivial, but the same figure, differently put, i.e. $425 per year seems too high. It is hard to make a habit to save every month. People will find thousand reasons why they can not save $35 every month and they will not find a single reason why they have to save $35 every month.

The preliminary reason for that is – this (figure above) is not how budget gets executed in most of the household. Average family or person do not expense what is left after saving, rather they will save the leftover after expenses. And in most of the cases, the reminder is a negative balance. Sadly true!

Your author genuinely wish that may God give you strength to fend off your impulse buys for expensive Cars, phones, Clothes and Other branded stuff. None of those expense by itself is harmful, but when they all add up, it pulls you towards the center of the gravity, which is way below the water level. And when you are at that level, it will probably be easy to go to the other side of the Earth, but it will be more difficult to come out of it. (Flat Earth community may cheer by this analogy, but my emphasis was on coming out of it)

Always try to live below your means. This is indeed number one step of financial independence.

2 – Invest The Saving

Let’s imaging you have the grit and passion to save at least the average amount or more. You cannot just keep collecting those cash under the mattress. Overtime, the cash devaluate. The purchasing power of cash decreases in the future years.

You have quite a few options to invest your saving like Real Estate, Treasury, Corporate Bonds, Stocks, Saving Accounts and so on. There are numerous studies about which investment is financially rewarding to investors and the result is pretty favorable to Stocks in a long run. So we are going to assume Stocks will be your method of deploying hard earned savings.

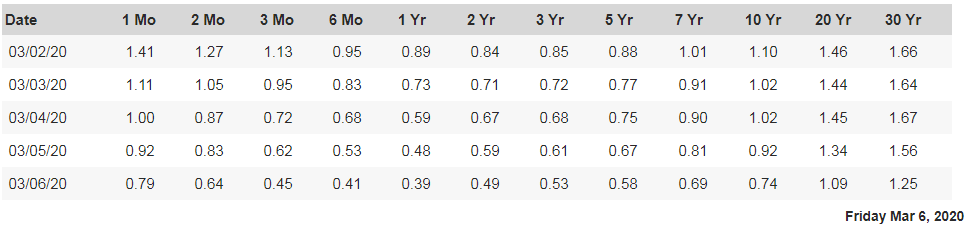

The current Treasury rates are listed in the table below. It seems bizarre to see 30 Year Treasury rate at 1.12 % while the Government is targeting inflation rate of 2%.

The top 500 publicly traded companies listed in US security Exchange, listed as S&P 500 Index, produce an average of 11% return per year. It might be lower than that in the future, but it will certainly be better than 1.25%.

Invest your Saving. Pick the investment vehicle which which will produce you a better result in a long run and that is – Investment in Stocks. Keep in mind that investing in Stocks means that you are investing in Business represented by that stock. You are a part owner of that Business. As trivial as it might be, you are the rightful owner of that company. Hello, Mr. owner!

3 – Diversify

It is extremely difficult to pick winning stocks. No one knows what derives the stocks performance in a short term. In a long run, however, it seems to follow the intrinsic value of the business. Benjamin Graham, the father of Value Investing, famously said, “In the short run, the market is a voting machine but in the long run it is a weighing machine”.

Here is the alarming index stats.

- 40 % of the stocks in S&P 500 go bankrupt in 20 years.

- 35 % of NYSE and Nasdaq stocks can be called unprofitable.

Furthermore, if you want to be a stock picker, your likelihood of picking a winner stock is only 60%. Overtime, most of the big business will become mediocre and very few of the small business become a giant. That is the nature of the business.

However, if you pick the entire index, you are concerned with overall index performance; therefore, individual stock performance do not matter much. Unless you spend 12 hours a day reading all sort of stuff including 10-Ks and 10-Qs, and have a heart of a stone, with no human emotions whatsoever, you cannot perform better than the index.

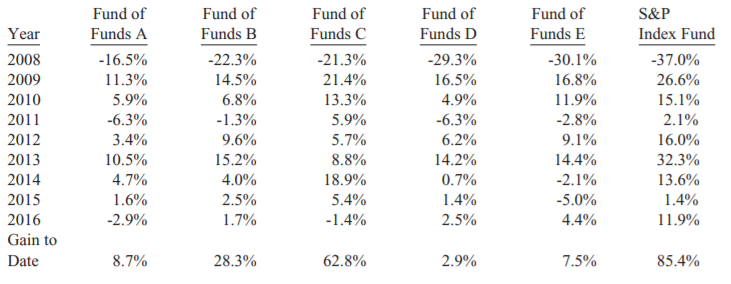

The figure above shows Warren Buffett’s famous bet against the best Mutual fund managers for 9 years. The best minds, not to mention with Harvard MBA, out there cannot even beat the super low, bond index. And statistics shows that most of the mutual funds do not beat the index fund.

You ain’t no Warren Buffett, so put that savings in S&P 500 index fund and let it compound for rest of your life. Boring yet best advice, which, apparently, only makes sense after a bit too late.

Don’t put all of your eggs in one basket. For the lack of a better word, Diversify. May be that is the word!

4 – Long Term

When a question was asked to Warren Buffett about when to sell a stock, he answered “never”. And that is what we mean when we say Long-term. Not 1, or 2, or 10, or 20 years, but your entire life time. As of 2019, the average life expectancy in United States is 78.9 years. If you start working and saving at 25 years old, you will have 53.9 years to invest and compound.

If you start saving at 25 years old and invest that saving in S&P 500 for 50 years, you are certain to retire as a millionaire. Although, a million after 50 years might mean a little, it is a great way to compound your little wealth. (We are assuming that S&P 500 will continue to produce an average return of 11% per year and your saving is adjusted for 2% inflation.)

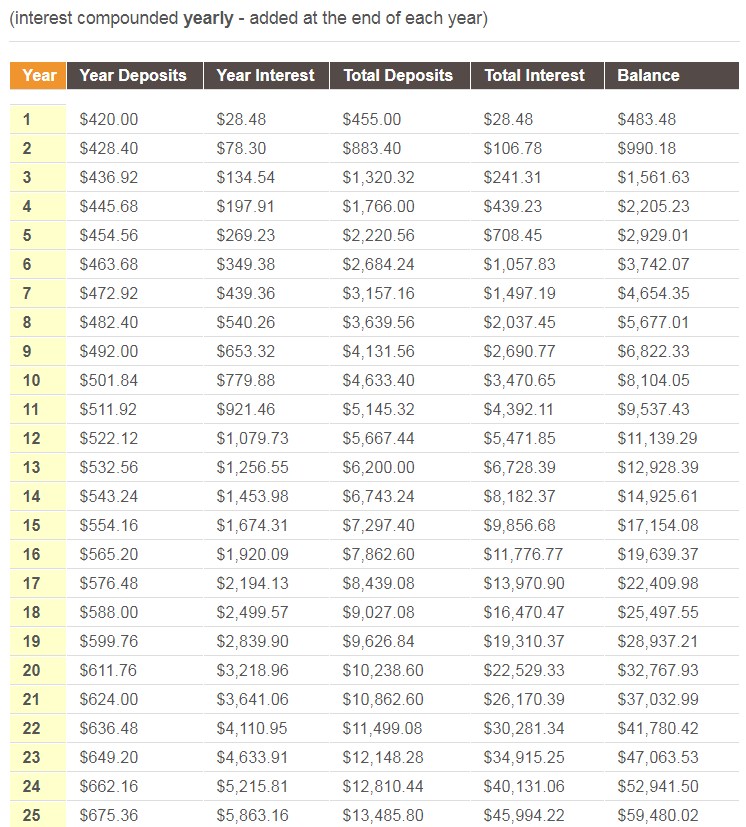

If you think 1 million is not enough, then invest $70 every month instead of $35. This way, you will have 2 million instead of 1 million. And if you think you need 10 million, then invest $350 per month and so on.

The windfall of this simple approach is dollar cost averaging. Dollar cost averaging is a strategy in which an investor places a fixed dollar amount into a given investment (usually common stock) on a regular basis. This strategy will let you buy more stocks when they are trading at discount. Not to mention the better sleep and a ton of time for other meaningful things.

Conclusion

The true value of wealth is not in its possession but in its use. In the process of creating wealth, if you stop living, you are not doing it right. What good does a $100,000 in your brokerage account do if all you do is staring at the stock market chart? Wealth unused might as well not exist.

Wealth doesn’t always mean pleasure and happiness. Darren Hardy describes it perfectly in the book “The Compound Effect”.

“The burdens of wealth are in the act of creating, the fear of keeping, the temptation of using, the guilt of abusing, the sorrow of losing, and the responsibility of handling it over to a succeeding generation.”

Live a little. You deserve it. If you have some wealth to invest, you are already better than the haft of the world’s population. Don’t pity or stress yourself. Wealth has nothing to do with happiness. Apparently, you will only realize it after you get wealthy!

Leave the restlessness and option trading for professionals.

If you follow the above common senses, you do not have to worry about short term market fluctuations because of variety of reasons like:

- Corona Virus/Pandemic

- Recession

- Depression

- Sales Miss/Beat

- Market Sentiment

- Oil Price fluctuation

- And so on…

More so, you will have time to do the right things like:

- Spend time with your friends and family

- Read

- Play soccer

- Or do the things that you love.

As I am writing this, the NYSE halts trading as stocks index plummeted. Dow is down $1,900 points, or 7%. Am I worried a bit? Nop. In-fact, I bought some business today in the Sell-off. (More on this in future post)

Current and prospective investors, please follow the common sense and live a little!

1 Comment