AT&T, a dividend aristocrat, is being part of our portfolio on and off for a long time. We have gained a good chunk of dividends as well as capital gain from owning this company.

Lately, it has been a drag. Partly due to pandemic, which has dented its media business. In the post split environment, where it is splitting its media business and combining with Discovery to form a new business, we evaluated the company again to see if it is still worth to hold on to it. And here is the summary of our conclusion.

AT&T’s main business is wireless service, which I am one of its customer. It is a reliable business since millions of Americans like myself pay the monthly fee for the phone and internet service. And occasionally, upgrade phones, which reinforces the stickiness of their customers to its network.

The reliable Wireless service carries 50% of its revenue and the rest of the 50% is a bad business, meaning the revenue is declining and profits are shrinking.

The current management is shrewd to get rid of a bad apple, however, you don’t get good price for bad apple. That is exactly what has happened with getting rid of the media business. The previous management should not have purchased it in the first place. Oh, well. 5 years too late.

Here are the examples of tossing good money to buy bad business. Fine examples of corporate managers with a huge ego to be the CEO of the biggest company!

- In July 2015, AT&T purchased DirectTV for $48.5 billion

- On October 22, 2016,AT&T announced a deal to buy Time Warner for $108.7 billion

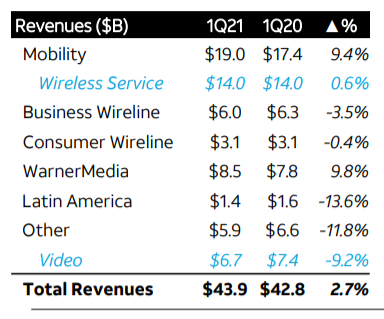

Here is the quarterly result prior to the Split-up.

Key Operating Metrics

| Total Operating Revenues | 2021-Q1 | 2020-Q1 | Change |

| Total Operating Revenues | 43,939 | 42,779 | 2.7 % |

| Operating Income | 7,661 | 7,486 | 2.3 % |

| Net Income | 7,942 | 4,963 | 60.0 % |

| Net Cash Provided by Operating Activities | 9,927 | 8,866 | |

| Capital expenditures, including $(61) and $(28) of interest during construction | (4,033) | (4,966) | |

| Free Cash Flow | 5,894 | 3,900 | |

| Long-Term Debt | 160,694 | 153,775 | |

| Total stockholders’ equity | 183,079 | 179,240 | |

| Total Liabilities and Stockholders’ Equity | 546,985 | 525,761 | |

| ROA | 1.5% | 0.9% | |

| ROE | 4.3% | 2.8% |

Anyway, AT&T does not have enough operating cash to continue the dividend payment of $14 billions each year. Now, they have two choices. First, to increase the cash flow and second, to cut the dividends. They chose the easiest one or perhaps the one they can handle easily.

Our initial investment thesis was solely based on the continuation of the current level of dividends payment. Now that it is confirmed that wont happen, we have only one choice i.e. to get out.

| Revised Dividends | Current Dividends | |

| Total Dividends | 2.4% | 5.1% |

| Capital Gain | 2.7% | 2.7% |

| Total Gain /w Dividends | 5.1% | 7.7% |

| Interest Provision (2.89% APR) | 42.6% | 28.1% |

| Tax Provision (25% Bracket) | 14.3% | 18.0% |

| Net Profit | 2.2% | 4.2% |

With the revised expected dividends, it is still expected to earn net 2.2% annually. I know this is very low return. Let us remind you that this is on margin, which adds to the its riskiness even more. Thus far, we felt like 2.2% net from other people’s money is a fine return.

Now, we feel a good night sleep is better than 2.2% return. Also, I think, we have found a better investment than this. You will hear on that shortly.

Goodbye, AT&T! We will miss your quarterly dividends.