“There is no shame in losing money on stock. Everyone does it. What is shameful is to hold on to a stock, or worse, to buy more of it when the fundamentals are detorating.” – Peter Lynch.

If you are one of the approximately 418,000 shareowners of General Electric (GE), the 127 years old American conglomerate, you certainly must have noticed it’s stock price. It’s not pretty. (see below)

My story as a GE investor is quite a phenomena. I first invested around 12K in 2015 based on this principle.

At one point my investment was up 30 plus percentage. At that time, GE paid around 4% dividends. Things were quite well. But, the honeymoon did not last too long.

I closed my position in not only a painful loss but also with the accord ‘My biggest loss thus far’ (Many big ones to come, certainly). I was down around 13K. It is all because of my stupidity. I think I deserved it.

What exactly did I do? Why did I close my position now?

My original acquired price was around $26. I have watched GE’s top line and nothing seemed odd to me. I should have thought deeply when Warren Buffett closed his position with GE. I was ignorant.

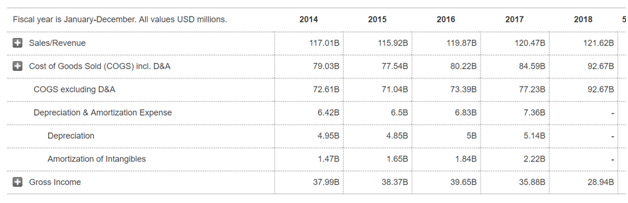

Rather, I bought more when the price slid to $24. I thought it is just a herd effect and it will recover. I couldn’t keep myself away from the anchoring and adjustment bias. Nothing seemed off to me when I see the revenue going up year over year (see figure above).

I outdid myself when I bought more of it when the price went down to $19 and $17. I was being a contrarian! I see blood on the street and was buying when everyone is selling. Believe me, you need an Iron-Gut to be a contrarian in the trading world. Being contrarian has a negative meaning when the crowd is rational.

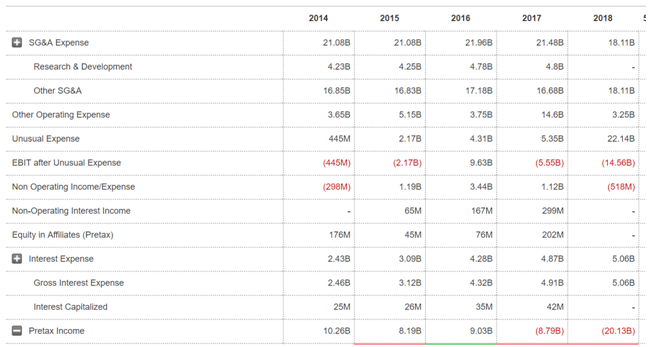

GE says it’s because of the unusual expense. It’s not unusual when it happens every year and is growing.

I finally regained my sense when I looked below the top line. Look at the pretax income. It’s blood red. From 9 billion profit to 20 billion loss in just two few years. GE says it is because of the unusual expense. It’s not unusual when it happens every year and is growing (see the figure below). This indeed would be a red flag had I looked at its financials.

GE operates in 8 different segments.

- Power

- Renewable Energy

- Oil & Gas

- Aviation

- Healthcare

- Transportation

- Lighting(*)

- GE Capital

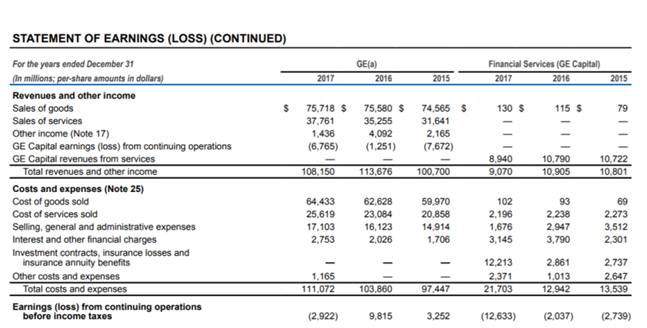

GE Capital seems to be the culprit (see figure below). GE Capital reported 12 billion loss in 2017. And that trend will continue for a few more years. Rest of the segments are quite alright.

If you are like me, who hates to read 10-K’s and 10-Q’s (especially the fine print), here is the abstract of what the GE managers are saying about this situation.

“During the fourth quarter of 2017, we completed the previously reported review of premium deficiency assumptions related to our run-off insurance operations (North America Life and Health (NALH)). With the completion of that review and NALH’s annual premium deficiency test, we recorded an increase to future policy benefit reserves of $8.9 billion and impairments of $0.4 billion of deferred acquisition costs and $0.2 billion of present value of future profits. This resulted in an after-tax charge of $6.2 billion to earnings in the fourth quarter of 2017.”

“As a regulated insurance business, NALH is subject to a statutory accounting framework for establishing reserves that requires the modification of certain assumptions to reflect moderately adverse conditions and other differences from the reserve calculation under GAAP. Under that framework, we estimate that GE Capital will need to contribute approximately $15 billion of capital to NALH over the next seven years. GE Capital plans to make a first capital contribution of approximately $3.5 billion in the first quarter of 2018 and expects to make further contributions of approximately $2 billion per year from 2019 through 2024.”

Honestly, I don’t quite understand why GE is booking billions of dollars in reserves (If you do, please help me understand it in the comment section). What terrible did GE capital do? Either way, it’s a hard-cash out of the shareholder’s pocket.

GE Capital paid common dividends to GE totaling $4.0 billion in 2017 compared with $20.1 billion in 2016. Cash generated from GE Industrial CFOA* amounted to $7.0 billion in 2017 and $9.9 billion in 2016, respectively, primarily due to:

- Net earnings for cash flows plus depreciation and deferred income taxes of $4.2 billion in 2017 compared with $14.1 billion in 2016.

- A decrease in cash generated from working capital of $1.2 billion in 2017 compared with 2016.

- GE Pension Plan contributions of $1.7 billion in 2017 compared with $0.3 billion in 2016.

GE couldn’t afford to pay 24 cents a share per quarter dividends. So they cut down the dividends. Since GE reduced its dividends to a penny per quarter, the dividend-seeking investors have already fled. Some Wall Streets experts, who saw this coming long before, are still trying to figure out what to do with their client’s money!

https://www.cnbc.com/amp/2018/12/18/the-man-who-called-ge-to-6point66-now-sees-this-ahead.html

Thankfully it’s not their own money.

Since GE reduce its dividends to a penny per quarter, the dividend-seeking investors have already fled.

There are seven big lawsuits going on including the SEC investigation of GE’s revenue recognition practices. This sounds like a big fee!

GE also announced that it plans to take actions to make GE Capital smaller and more focused, including a substantial reductionin the size of GE Capital’s Energy Financial Services and Industrial Finance businesses over the next 24 months.

In a long term, I firmly believe GE will be great again (my completely subjective feelings). Its core business (Industrial segment) is the backbone of the world. A lot of industries like Healthcare, Power, Oil, and Aviation heavily depend on GE. It has thousands of patents which apparently are its real moat. They will dispense a lot of cash for a long time. However, the short term is a mess.

I estimate GE is trading at around 10 times the forward earnings. If it trades at around 8 times forward earnings, I will consider buying it.

Disclaimer – No position.

Some Good Reads

- How Value Investing made Warren Buffett the best investor? (CNBC)

- How value investing can add value to your money (Economic Times)

- Value Investing Portfolio (Seeking Alpha)

1 Comment