My better is better than your better. – Nike.

Nike Inc. reported its Fiscal 2022 Q2 results and here are the summary:

- Revenue up 1% to $11.4 Billion

- Direct Sale up 9%

- Gross Margin up 280 basis points to 45.9%

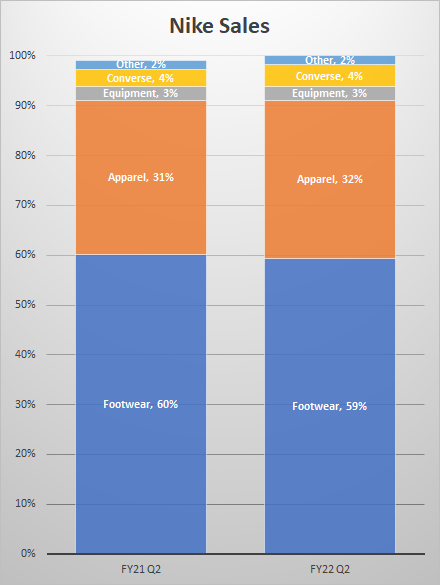

Sales in North America and Europe was up 21% and 22% respectively. However, China and Asia pacific were down 36% and 8% respectively. Per the management, Inventory played the role on both the market. The decline was largely due to lower levels of available inventory resulting from COVID-19 related factory closures. North America’s growth was due to higher levels of in-transit inventory entering the second quarter.

Since North America and Europe contributes most to the revenue and earnings, Nike reported a solid quarter.

Their consumer direct focus enabled them to increase the gross margin by 280 basis points. Nike Direct grew 8% including record Black Friday week.

Their selling and administrative expense was up 15% due to higher strategic technology investments, which should benefit Nike in a long term.

Here is the Q2 Y/Y Sales comparison.

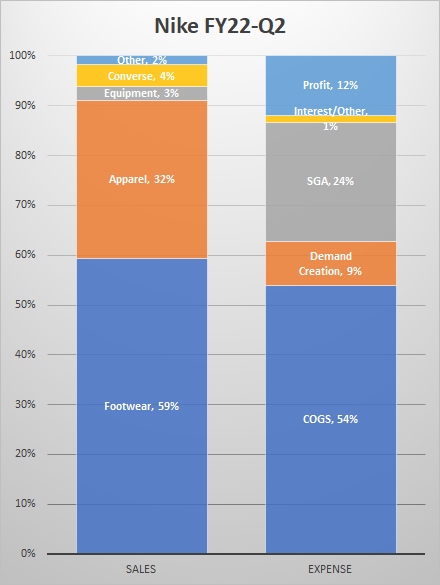

Here is the summary of their Sales and Expenses.

All in all, the second quarter reflect the deep consumer connections, the continued strength of our brands and strong marketplace demand, per Matt Friend, EVP.

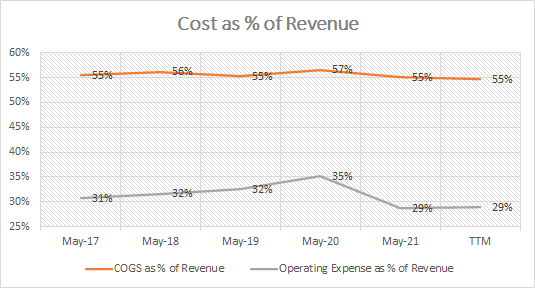

This graph below tells you how consistent Nike Business is. For the last 5 years, the Cost of revenue is quite flat. It is around 55% of the Revenue. And the management is getting better and better. Year 2020 saw some spike in operating expense because of the COVID-19 pandemic.

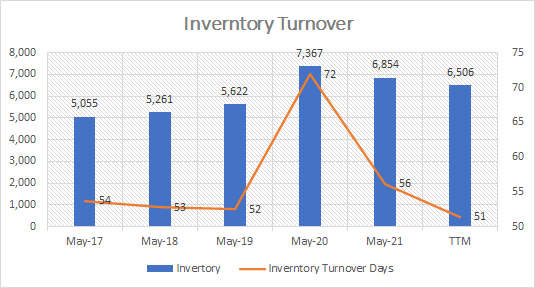

Nike’s distribution channel is also getting better every year. With the exception of last year, the inventory turnover days are getting better. Currently, on average they sell all their inventories within 51 days.

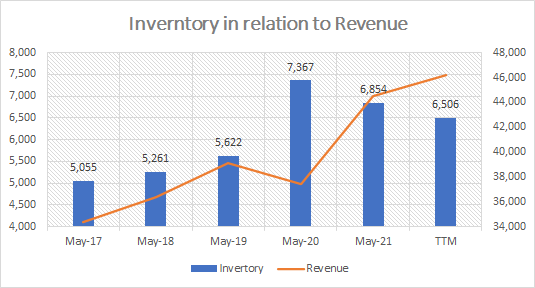

Below inventory and revenue numbers are in millions.

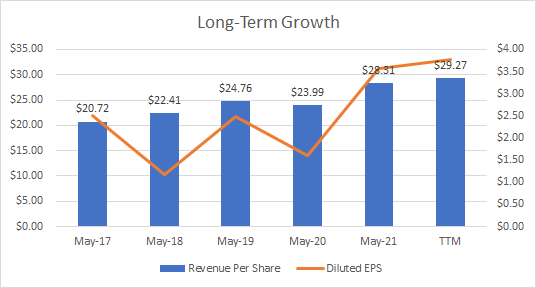

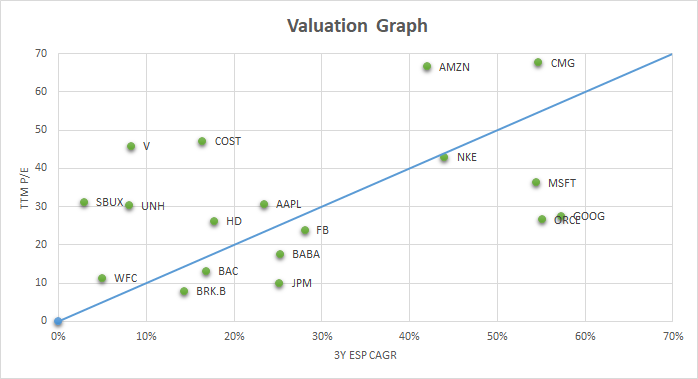

Currently, Nike sells at PE of 43. This seems quite expensive. However, with the 3Y EPS compounded annual growth rate of 44%, it is relatively priced. Here is the visual representation of where Nike sits relative to other well known brands.

Nike is in the borderline of being expensive stock. It ought to go down, just like my Cholesterol level! Nike got to increase the earnings or stock price should fall. Which one will outdo – no one knows. Not even me!

Although, the market reacted quite well after the quarterly result was out, Nike is clearly under-performing the S&P 500 YTD. See below.

With dividends of $437 million, up 14% from the prior year and share repurchases of $968 million for the quarter, Nike has been a satisfactory holding for us and it sits pleasantly in our portfolio for now.